Chip Eng Seng (CES) is one of the construction stocks within my

portfolio. CES had commenced a series of buy-backs activities lately. Share

buy-back is normally conducted when (a) Management feel that their stock is

undervalued on open market (b) Provide bonus incentive compensation plans for

employees (c) Protect the company against a takeover threat. Not entirely sure

the reason in this case, but hopefully it is for reason stated in (a) and investors will stand

to benefit.

portfolio. CES had commenced a series of buy-backs activities lately. Share

buy-back is normally conducted when (a) Management feel that their stock is

undervalued on open market (b) Provide bonus incentive compensation plans for

employees (c) Protect the company against a takeover threat. Not entirely sure

the reason in this case, but hopefully it is for reason stated in (a) and investors will stand

to benefit.

Share Buy Back

Since 1Q14 results announced, there are four buybacks in June and one in May. This month, 2.83mil shares were bought back at

S$0.755 while 2.23mil shares were bought back at S$0.739 last month. Since End

Mar 2014, the Company held 25.48mil treasury shares. Including the buybacks, Treasury

shares increased to 30.54mil. As of today, total treasury shares are close to 5% of the 642mil

issued shares held as of end Mar 2014.

S$0.755 while 2.23mil shares were bought back at S$0.739 last month. Since End

Mar 2014, the Company held 25.48mil treasury shares. Including the buybacks, Treasury

shares increased to 30.54mil. As of today, total treasury shares are close to 5% of the 642mil

issued shares held as of end Mar 2014.

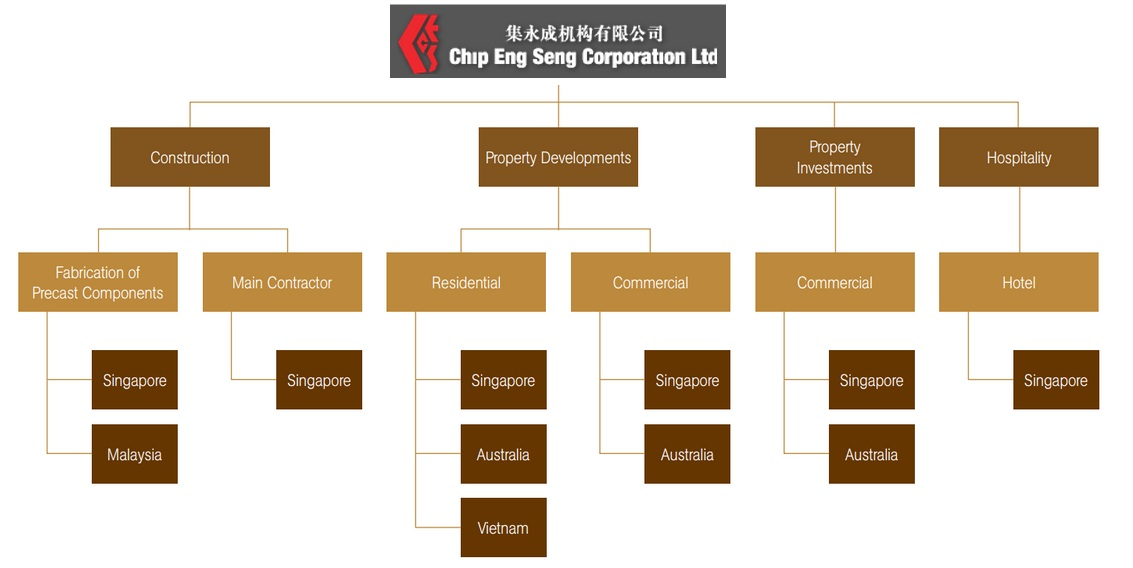

Company Brief

Founded in 1960 and listed in SGX in 1999, CES business includes Construction and Property. The construction

arm completed many private and public projects notably Duxton at Tanjong Pagar.

Ongoing projects include both public and private residential development and

constructions projects locally and regionally. The construction projects are also supplemented by its very own fabrication of pre-cast components. CES has also won

the “Most Transparent Company – Construction Category”, over the past few

years. Chairman and Founder Lim Tiam Seng and his brother Dy Chairman Lim Tiang Chuan are

majority shareholders owning a total of ~16% of the company shares.

arm completed many private and public projects notably Duxton at Tanjong Pagar.

Ongoing projects include both public and private residential development and

constructions projects locally and regionally. The construction projects are also supplemented by its very own fabrication of pre-cast components. CES has also won

the “Most Transparent Company – Construction Category”, over the past few

years. Chairman and Founder Lim Tiam Seng and his brother Dy Chairman Lim Tiang Chuan are

majority shareholders owning a total of ~16% of the company shares.

Recent Contract Win

Two weeks ago Chip Eng Seng announced a $165

million HDB contract for building works at Sembawang Neighbourhood 1

Contract 10. Slated to be carried out over a course of 36 months, the newly

awarded contract encompasses the construction of 8

residential blocks, housing a total of 1,220 dwelling units together

with other community facilities and is tentatively expected to be completed in

the second quarter of 2017.

million HDB contract for building works at Sembawang Neighbourhood 1

Contract 10. Slated to be carried out over a course of 36 months, the newly

awarded contract encompasses the construction of 8

residential blocks, housing a total of 1,220 dwelling units together

with other community facilities and is tentatively expected to be completed in

the second quarter of 2017.

As at 31 March 2014, the Group’s order

book stood at $453 million. Factoring in this

latest contract win, the Group’s order book rises to $618

million.

book stood at $453 million. Factoring in this

latest contract win, the Group’s order book rises to $618

million.

Fundamentals

- Price S$0.765 ; Mkt Cap S$487.3mil

- PE 6.8 (based on 2013 EPS) / PE 5.7

(based on annualized 1Q EPS of 3.35c) - PB 0.99 (base on 2013 NAV of 77.12c) / PB 0.94 (base on 1Q14 NAV of 81.59c)

- Dividend Yield 4c for past 4 years.

This translate to 5.2% yield at current price of 0.765. - Has healthy cash and equiv of S$191mil as of End Mar 14.

- Net Debt (total liabilities subtract cash) to Equity =1.44. Sllightly high.

- Current Ratio (current assets / current liabilities) =2.2. Relatively healthy.

Looking Ahead

Moving forward, the Group will continue to participate in land tenders

for property developments in

for property developments in

Singapore and will continue to look for opportunities to replenish its

land bank in Singapore and the

land bank in Singapore and the

surrounding region.

Below is a summary referring to an excerpt from analyst report from NRA on 24 Apr 2014. Base on the forecast, 2014F PE ratio is only 2.7.

Record revenues to be recognised this year.

The group will recognise revenues and related costs upon TOP for 3

projects in FY14. They include Alexandra Central, Belvia, and 100 Pasir Panjang

and which we estimate would contribute around 65% of the record S$1.3b expected

revenues in FY14. It will also fully recognise 40% of profits from Belysa.

projects in FY14. They include Alexandra Central, Belvia, and 100 Pasir Panjang

and which we estimate would contribute around 65% of the record S$1.3b expected

revenues in FY14. It will also fully recognise 40% of profits from Belysa.

Hotel

Hotel business to provide recurring revenues. Its hotel at Alexandra

Central is expected to be completed in mid-15 and will begin to provide a

steady recurring revenue stream to the group from 2H15 onwards. Although we

estimate it will provide only around 5-10% of total group revenues in our

forecast period, we believe it is a milestone for the group’s effort to

diversify into the hospitality sector

Central is expected to be completed in mid-15 and will begin to provide a

steady recurring revenue stream to the group from 2H15 onwards. Although we

estimate it will provide only around 5-10% of total group revenues in our

forecast period, we believe it is a milestone for the group’s effort to

diversify into the hospitality sector

Australia property demand

Riding on firm Australian property demand. It successfully launched its

first property in Australia back in 2012 with the 33M at 33 Mackenzie Street, Melbourne.

It is currently developing Melbourne’s tallest CBD residential building – the

Tower Melbourne. The 71 floors Tower Melbourne was 99% sold as at the end of

4Q13. The group is expected to launch another new development project in

Doncaster, Australia later this year.

first property in Australia back in 2012 with the 33M at 33 Mackenzie Street, Melbourne.

It is currently developing Melbourne’s tallest CBD residential building – the

Tower Melbourne. The 71 floors Tower Melbourne was 99% sold as at the end of

4Q13. The group is expected to launch another new development project in

Doncaster, Australia later this year.

Rolf’s View

Read a book called Contrarian Investment Strategies by David Dreman. One of the Rules states:

“Buy solid companies currently out of market favor, as measured by their low Price- to-Earnings, Price-to-Cash Flow or Price-to-Book ratios, or by their high yields.” – David Dreman

CES low PE of 5.7, a tad discount to Book value and annualized yield of 5.3% may worth considering. Industry average PE for Construction and Property is approx. 7 and 7.7 respectively. Of course, there is risk of Singapore’s property market facing imminent danger of slowdown, thus affecting companies in the property and building sector.

Related Post:

Nice knowledge gaining article. This post is really the best on this valuable topic. buy cbdoils

I found your this post while searching for information about blog-related research … It's a good post .. keep posting and updating information. where tobuy cbd wax online shopping

CBD hemp oil, would like to find out more about CBD.http://www.cbddogtreats.org/

What's more, it's advisable to check with a professional before consuming CBD oil for absolutely any medical condition, especially anxiety. http://www.cbdspray.org/

I need to to thank you for this very good read!! I definitely loved every little bit of it. I have you bookmarked to check out new things you post… convert psd to wordpress theme

As soon as it's surely a great situation to make CBD oil easily readily available for people throughout the planet. You can find more details on hempoilforpain on the site http://www.hempoilforpain.net/contacts.

It's beneficial to obtain an idea about what the several دكتور نفسي

your doctor orders for you are for.

This is such a great resource that you are providing and you give it away for free. I love seeing blog that understand the value of providing a quality resource for free. topdogcbd

The next time I read a blog, I hope that it doesnt disappoint me as much as this one. I mean, I know it was my choice to read, but I actually thought you have something interesting to say. All I hear is a bunch of whining about something that you could fix if you werent too busy looking for attention. Webtalk Invite